Data Brief 2020-027 | November 6, 2020 | Written and compiled by Leila Gonzales and Christopher Keane, AGI

Download Data Brief

COVID-19 Impacts to Geoscience Businesses (Summer – Fall 2020)

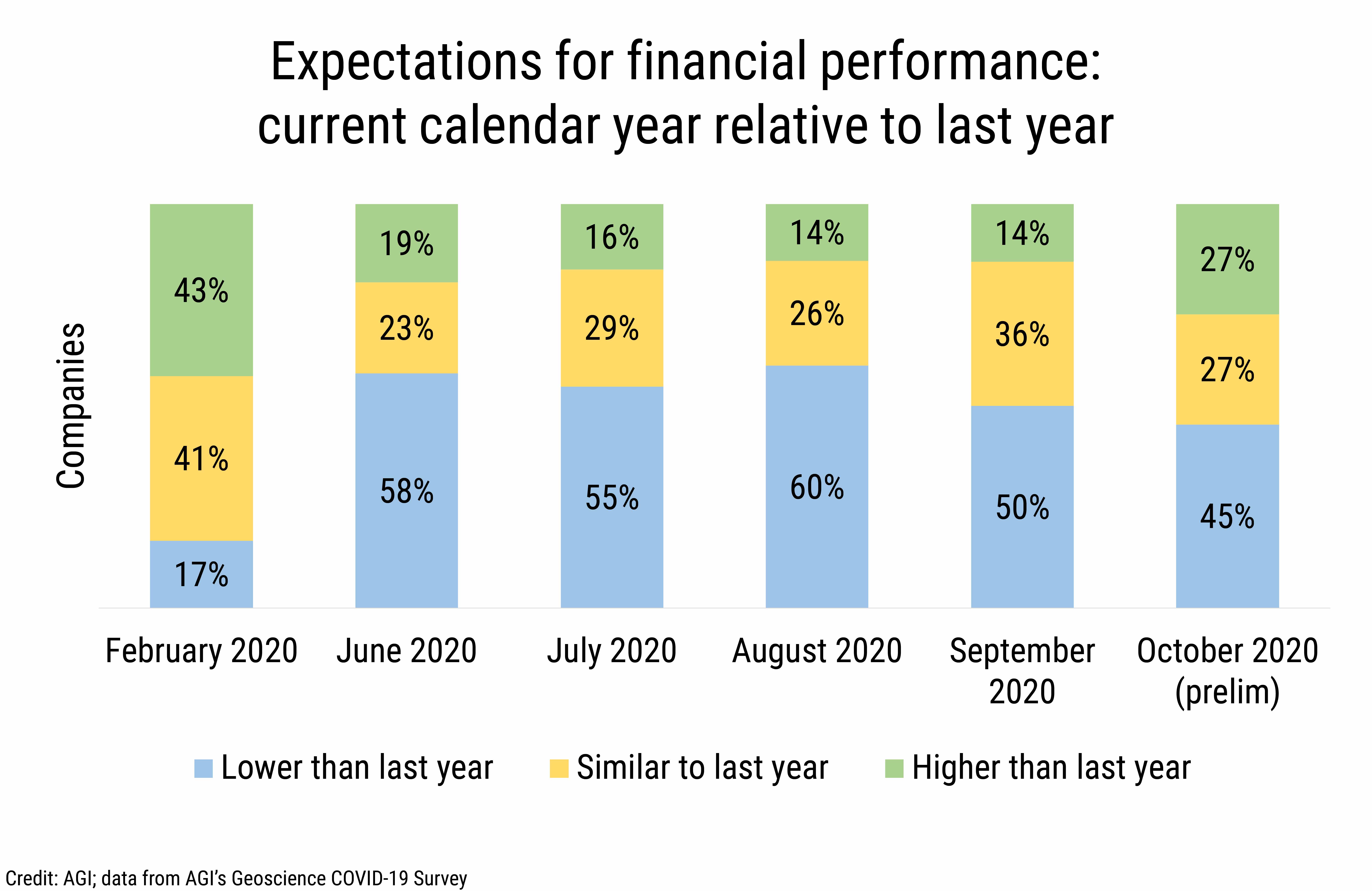

Throughout the summer, over half of geoscience employers reported

expectations of lower financial performance relative to 2019. In

September, this percentage improved to 50% and preliminary data from

October indicates continued improvement in financial performance with

only 45% of companies expecting lower performance relative to 2019. Over

the same period, the percentage of companies reporting either similar or

better financial performance relative to 2019 steadily increased from

42% in June to 55% in October.

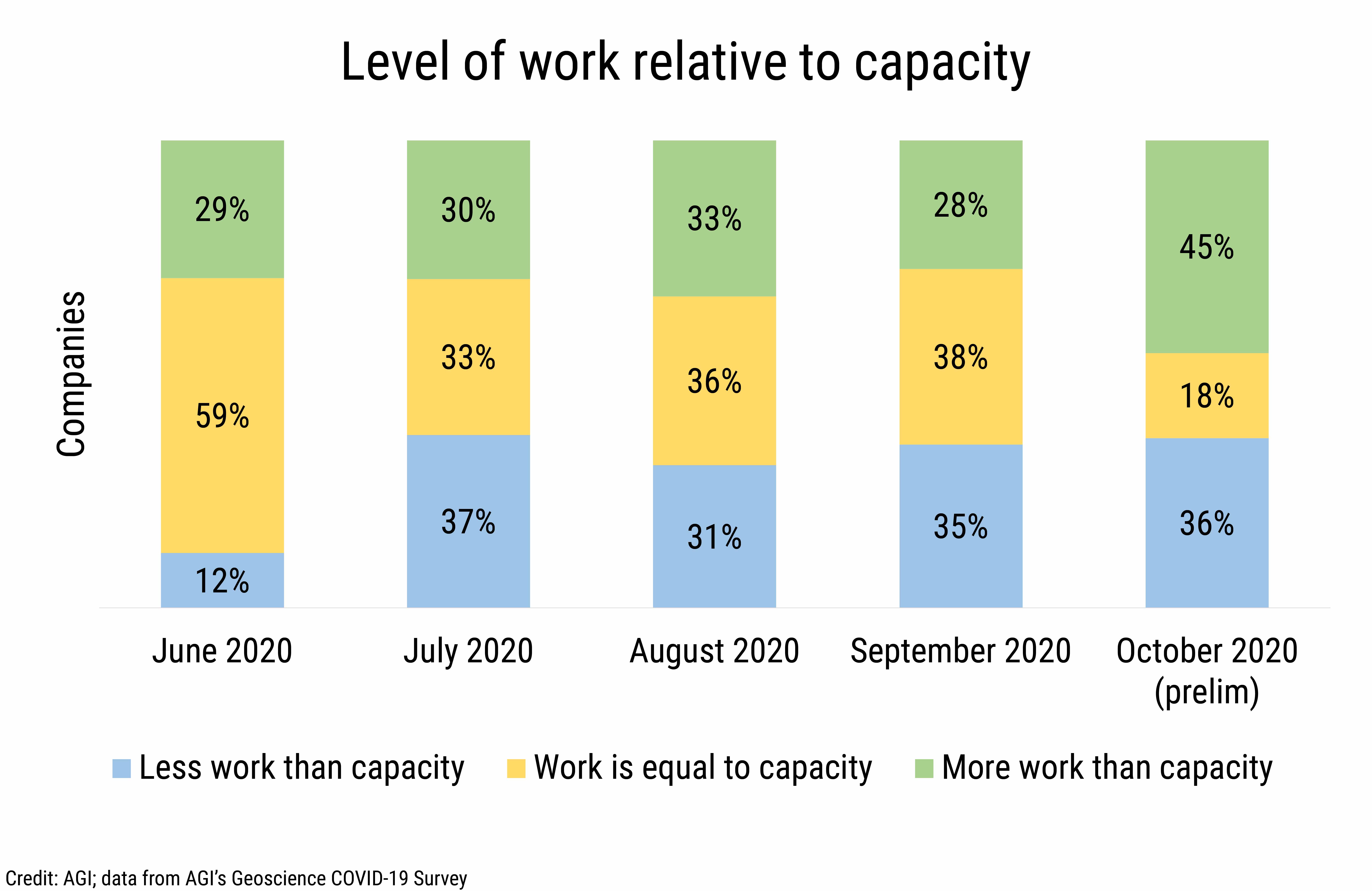

Since June, approximately 30% of companies reported increased workloads

relative to staffing, and preliminary data from October indicates this

percentage has increased to 45%. Meanwhile, the percentage of companies

reporting decreased workloads relative to staffing has remained

relatively steady since July despite the uptick in productivity in

October.

DB_2020-027 chart 01: Expectations for financial performance: current calendar year relative to last year (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2020-027 chart 02: Level of work relative to capacity (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

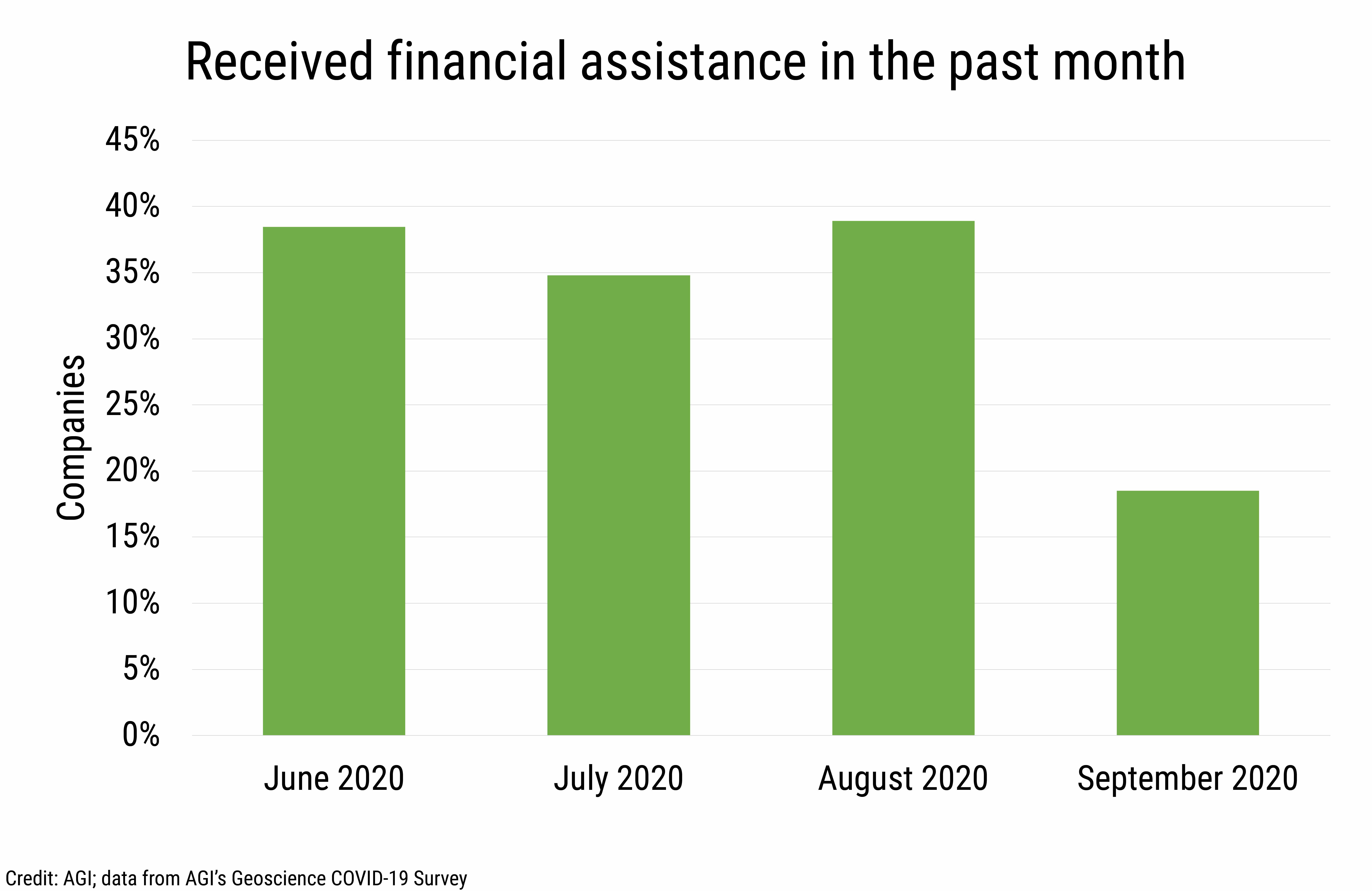

Over the summer, just over one-third of companies reported receiving

financial assistance, and this percentage dropped to 19% in September.

Of those companies specifying the types of financial assistance

received, the vast majority reported receiving federal aid such as from

the Paycheck Protection Program (PPP), Economic Injury Disaster Loan

program (EIDL) or SBA Loan Forgiveness program. With the end of the PPP

in August, we see a concurrent drop in the percentage of businesses

receiving financial aid.

Due to the end of the PPP and the decline in companies reporting

financial assistance in September, in October’s round of surveying, we

did not ask employers if they received financial assistance in the past

month, but instead asked if the end of the PPP resulted in a change to

business operational strategies. Preliminary data indicates that

although federal aid was useful, the end of PPP did not change business

operational strategies. This also aligns with the improvements in

financial performance and productivity discussed earlier in this data

brief.

Strategies used by geoscience employers for dealing with COVID-19

impacts have predominantly focused on investment in remote work

technologies followed by implementation of health and safety protocols

for those working in facilities, offices, and at field sites. Some

companies noted increased communication, cooperation and cohesiveness as

a result of the switch to online technologies, and others noted more

frequent and focused internal and external communication with colleagues

and clients. In addition, some companies noted that they may be

considering a shift towards more permanent telework with limited

in-office attendance even after the end of the COVID-19 pandemic.

DB_2020-027 chart 03: Received financial assistance in the past month (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

Most of the health and safety protocols implemented by companies

includes standard COVID-19 protocols for social distancing, disinfection

of surfaces and shared equipment, mask wearing, reduced staffing and/or

cohorts, etc., in addition to guidelines on vehicle usage. Some

companies noted that they are taking the time to increase marketing and

networking activities, including re-establishing connections with

former clients and prospecting for new work with existing clients, and

others have noted that they are taking advantage of contracting

opportunities that would otherwise be taken by seasonal staff.

Additionally, maintaining budgetary discipline is another strategy

mentioned by some companies.

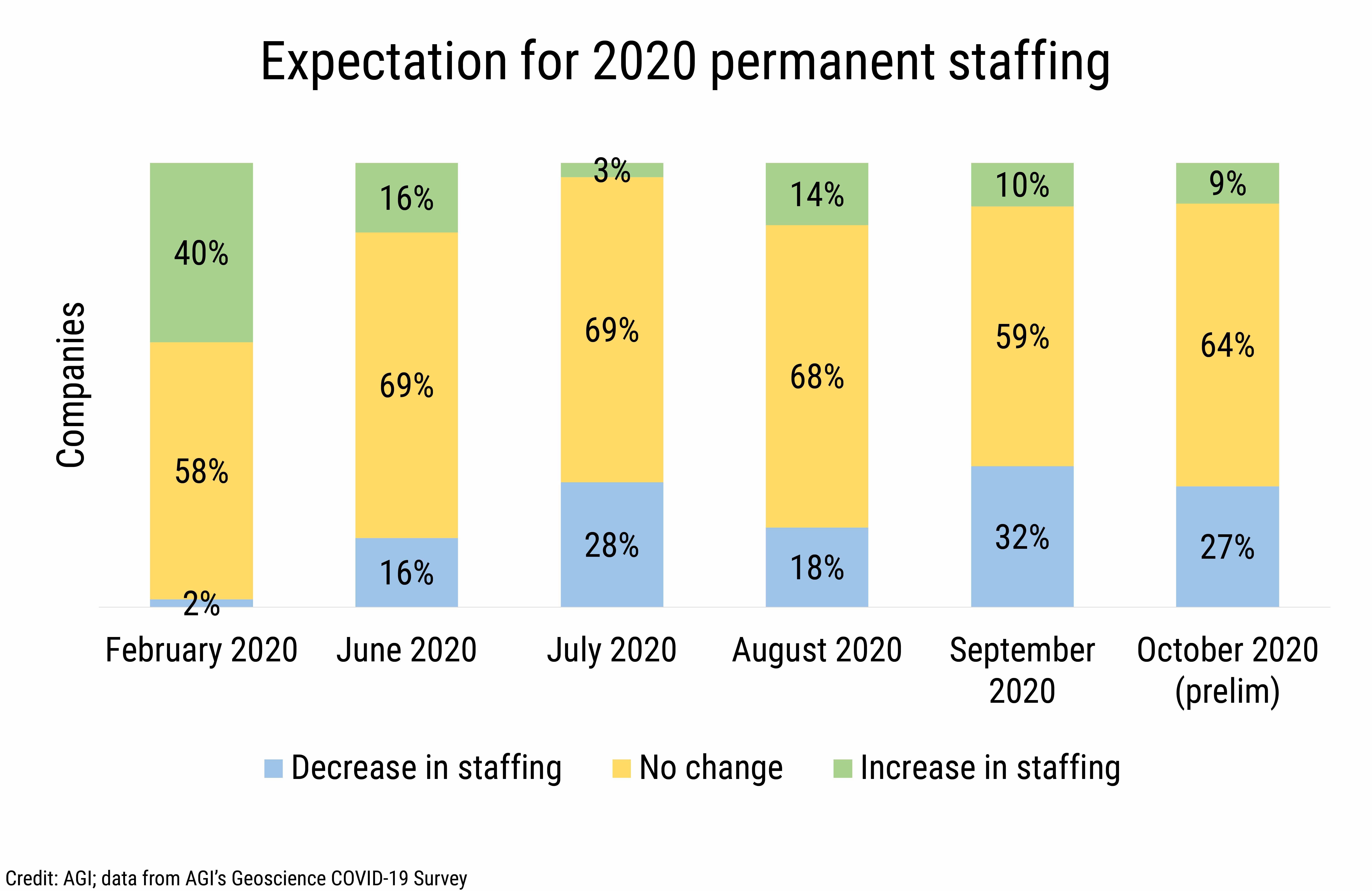

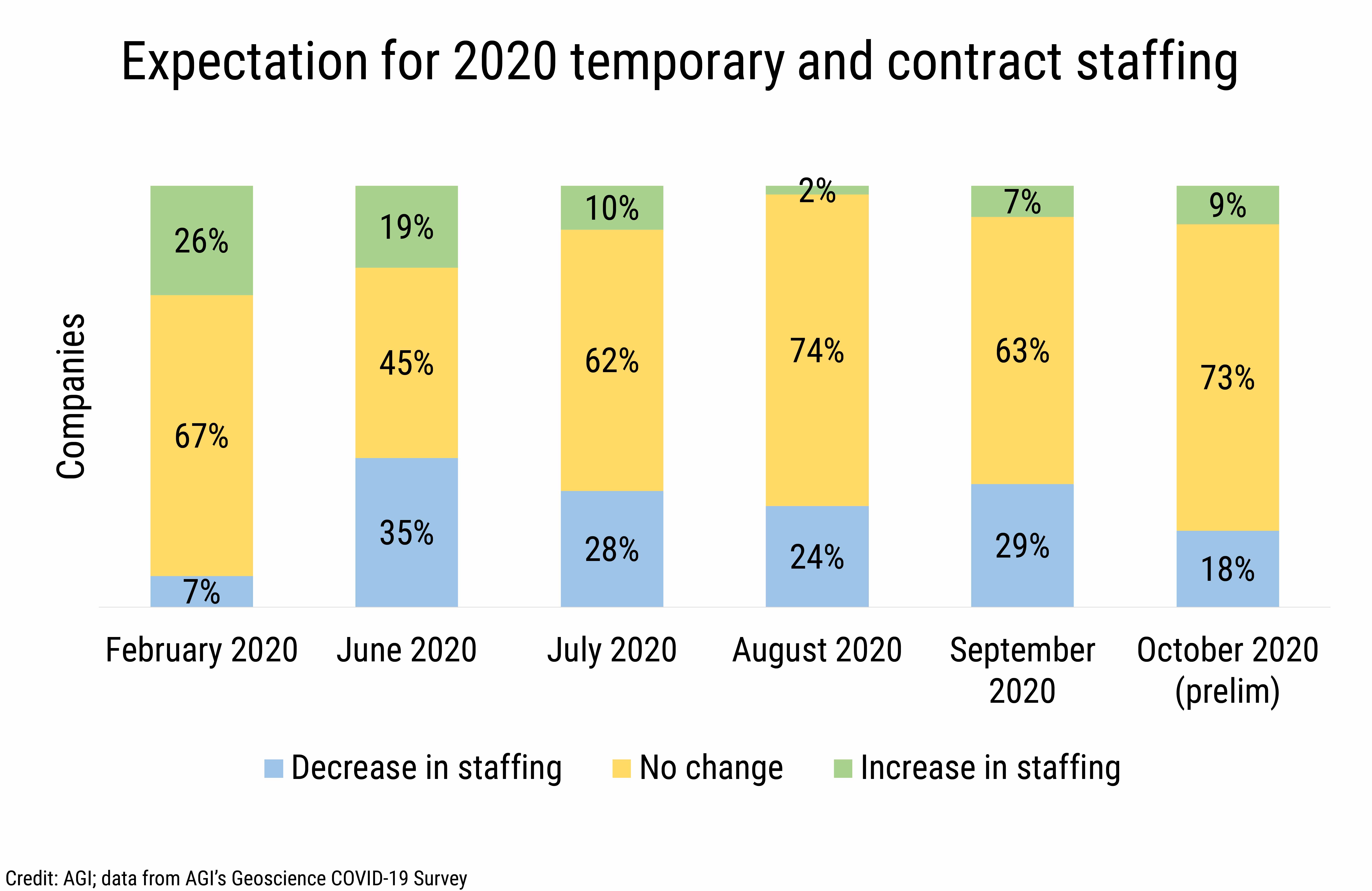

Staffing

While most companies expect no change in permanent staffing this year,

the percentage of companies reporting expected decreases in permanent

staffing has fluctuated between 16% and 32% since June. Similarly, while

most companies reported no expected changes in temporary or contract

staffing, the percentage of companies expecting decreases in temporary

and contract staffing declined from 35% in June to 18% in October.

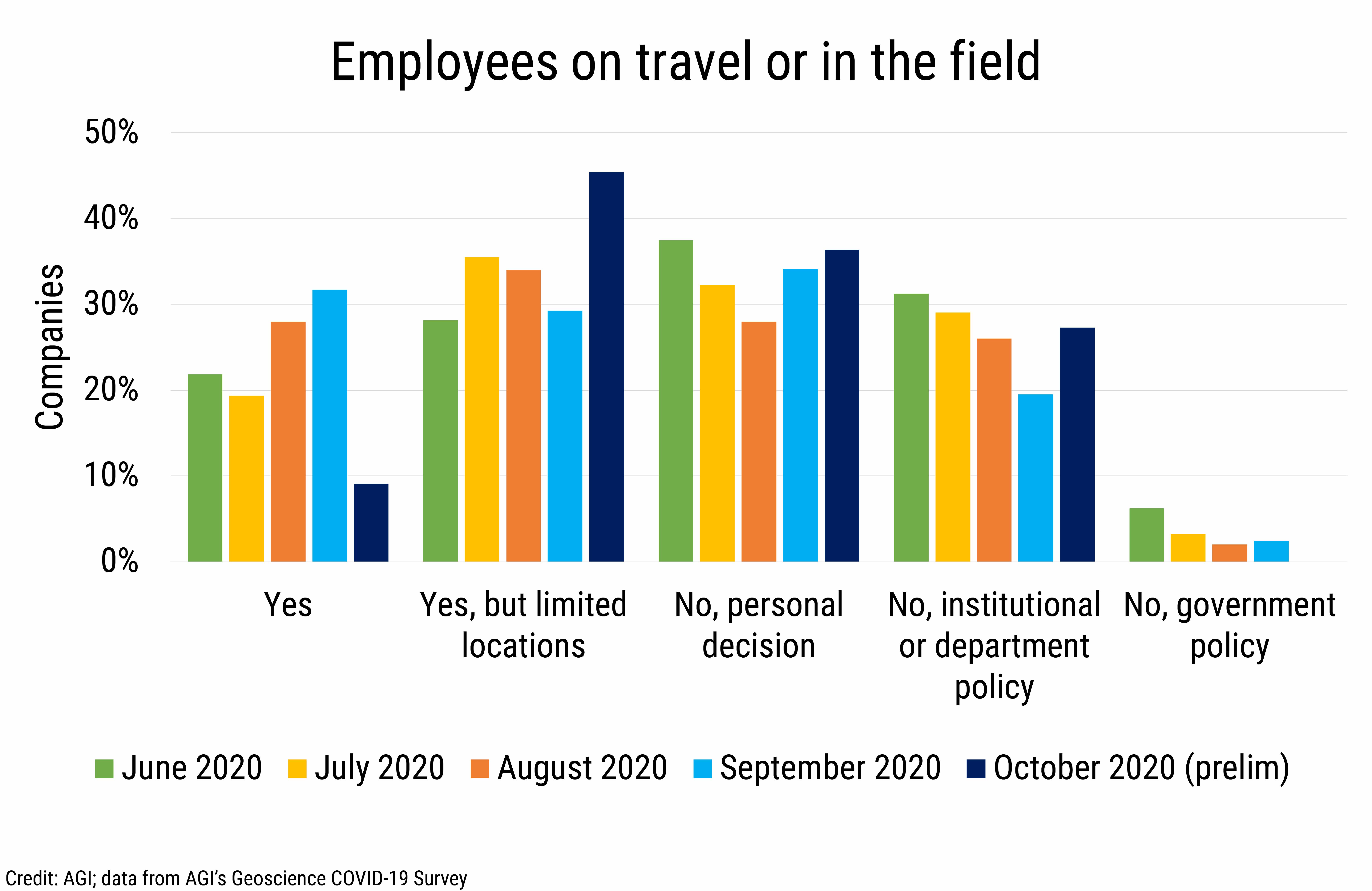

In June, half of businesses reported that they had employees that were

either on travel or working in the field and this increased to 56% in

September, there after dropping to 45% in October. Preliminary data from

October also indicates an increase in the percentage of businesses

reporting that employees were not travelling or conducting field work

due to either institutional / departmental policies or due to their own

personal decisions – the latter an increasing trend since August.

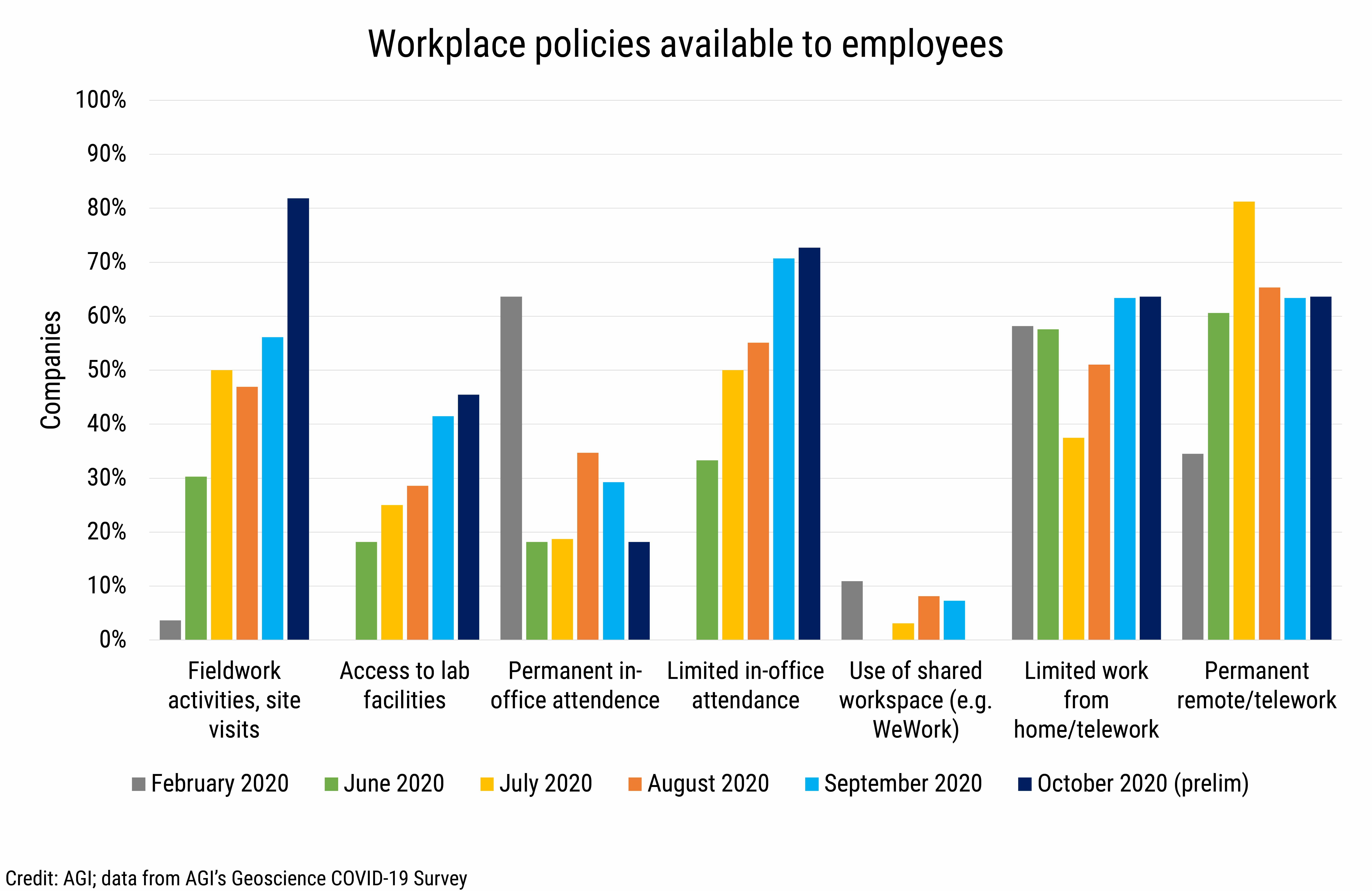

Workplace policies available to employees have shifted as companies have

adjusted to long-term remote work situations and since June over 90% of

companies provided limited and/or permanent telework situations for

their employees. The percentage of companies providing employees with

the ability for limited work in the office has continued to increase,

from 33% in June to 73% in October while the percentage of companies

that have provided employees with the ability for permanent in-office

work declined from 33% in August to 18% in October. The percentage of

companies providing employees with access to lab facilities, fieldwork

and site visits have continued to increase since June.

DB_2020-027 chart 04: Expectation for 2020 permanent staffing (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2020-027 chart 05: Expectation for 2020 temporary and contract staffing (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2020-027 chart 06: Employees on travel or in the field (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2020-027 chart 07: Workplace policies available to employees (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

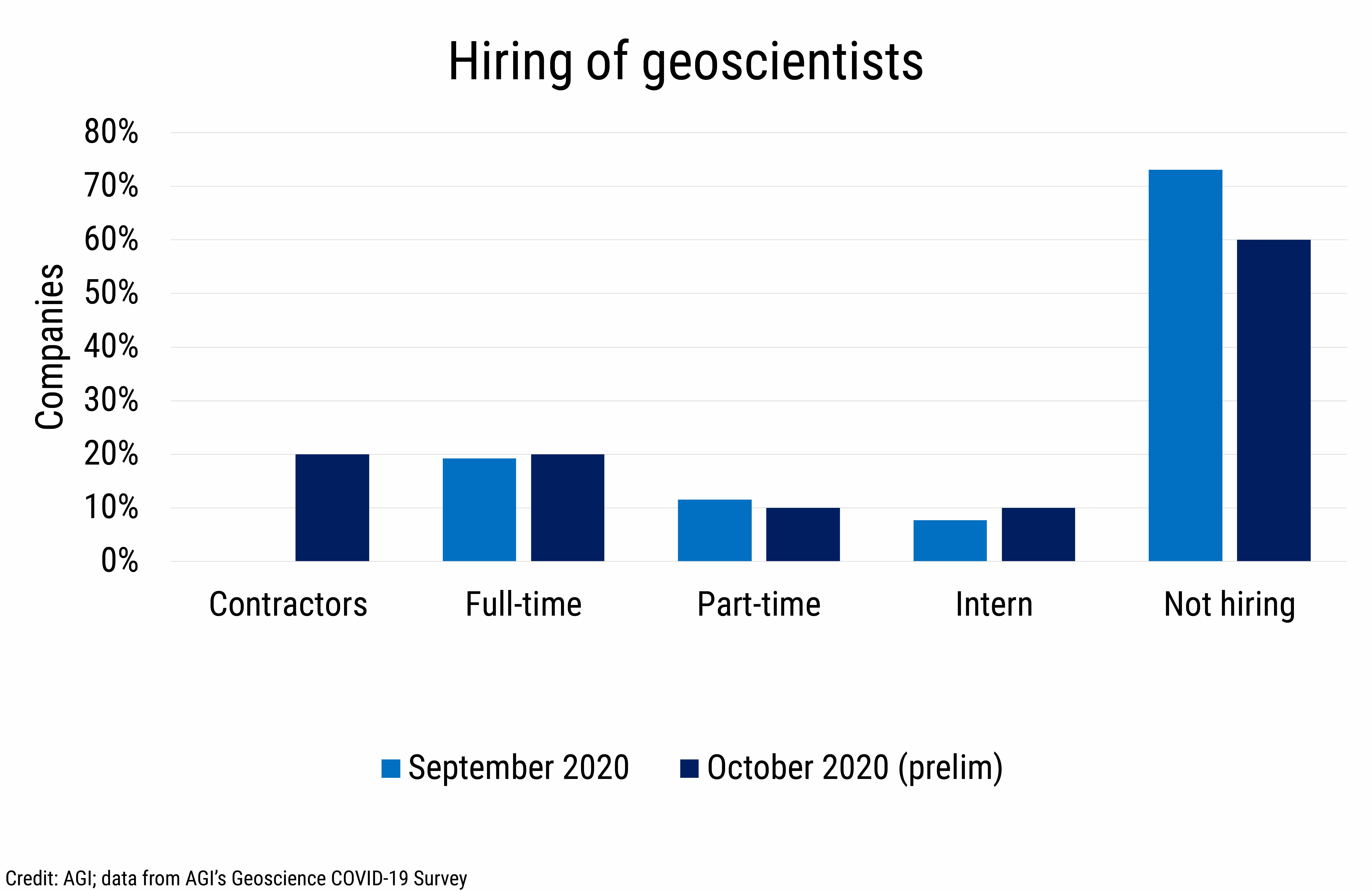

Hiring Trends

Starting in September, we began asking employers questions regarding

job openings and hiring trends. While most employers are not hiring,

there has been an increase in the percentage of companies reporting job

openings since September (27% to 36% in October) in addition to those

hiring geoscience employees

DB_2020-027 chart 08: Hiring of geoscientists (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

In addition to asking about hiring trends, we also inquired about

challenges employers are facing in terms of hiring and recruiting new

talent as well as about how the pandemic may have changed what employers

are looking for in potential candidates. Some employers reported that

budgetary restrictions such as hiring freezes and limited resources

affected their ability to hire new talent, while others indicated that

there were a lack of qualified candidates for available positions and a

decreased ability to network to find new talent. Other employers

indicated having to pass up candidates who only wanted work-at-home

arrangements and would not consider positions that required onsite work

either in the office or lab. Other challenges included issues with

online interviewing not being as effective as face-to-face interviews,

and challenges with the new hire onboarding process in regards to

integration with the company’s culture and core values.

Skills and training that employers have stated they are looking for in

new hires include the ability and motivation to learn and adapt to new

projects and tasks, technical proficiency and experience applicable to

specific projects, ability to work independently and in project teams,

and the ability to fit into the company’s organizational culture. In

addition, several employers indicated that although they typically hire

master’s and bachelor’s level graduates, they also hire doctorates.

Most employers indicated that the pandemic has not changed what they are

looking for in employees; however, some employers indicated that the

pandemic has made them look more closely at candidates that can

demonstrate that they can work independently without supervision. Other

employers indicated that they have become more selective in their hiring

as a result of the pandemic.

We will continue to provide current snapshots on the impacts of COVID-19

on the geoscience enterprise throughout the year. For more information,

and to participate in the study, please visit:

www.americangeosciences.org/workforce/covid19

Funding for this project is provided by the National Science Foundation

(Award #2029570). The results and interpretation of the survey are the

views of the American Geosciences Institute and not those of the

National Science Foundation.