Data Brief 2022-002 | January 17, 2022 | Written and compiled by Leila Gonzales and Christopher Keane, AGI

Download Data Brief

COVID-19 Impacts on Geoscience Business Operations Through 2021

In 2021, geoscientist-employing organizations’ financial performance

expectations shifted positively relative to 2020. In January 2021,

nearly two-thirds of employers expected their financial performance for

the year would be similar or higher than 2020, and by December 2021, 88%

of employers reported the same. The percentage of employers reporting

lower financial performance expectations relative to 2020 dropped from

36% to 12% between January and December 2021.

In February 2020, 76% of employers expected their financial performance

for the year would be similar or higher than 2019. This sharply changed

once the pandemic began with 50% or more of employers expecting worse

financial performance through December 2020. Financial outlook improved

markedly with the release of vaccine programs and economic reopening

during 2021. During 2021, over half of employers expected their

financial performance to be similar or higher than 2020 as well as than

before the pandemic. By December 2021, 75% of employers reported they

expected their financial performance level to improve relative to before

the pandemic.

DB_2022-002 chart 01: Expectations for financial performance: current calendar year relative to prior year (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2022-002 chart 02: Expectations for financial performance: current calendar year relative to prior year and pre-pandemic (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

Productivity

Since June 2020, most employers have reported full or excess workloads

relative to staffing levels. In 2021, the percentage of employers

reporting excess workloads relative to staffing rose from 29% in January

to 52% in December. For comparison, in 2020 the percentage of employers

reporting excess workloads relative to staffing ranged from 25% to 37%.

The percentage of employers reporting excess staffing capacity in 2021

declined from 44% in January to 24% in December, with the lowest

percentages occurring in August and September (20% and 19%,

respectively).

DB_2022-002 chart 03: Level of work relative to capacity (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

Financial Assistance

In July 2020, 44% of employers reported receiving some form of financial

assistance, thereafter declining to 15% by the end of the year. Federal

assistance was the primary type of aid received, followed by state and

local aid, and then investment by business owners into their companies.

In 2020, the primary form of aid received in July and August was federal

assistance in the form of loans through the Paycheck Protection Program

and Economic Injury Disaster Loans (EIDL). In 2021, aid from the

American Rescue Plan boosted between 23% to 40% of employers from Spring

through late Summer in the form of federal, state and local assistance.

DB_2022-002 chart 04: Received financial assistance in the past month (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

Business Operations Impacts

Employers have increasingly reported no pandemic-related impacts to

business operations since 2020, with two-thirds of employers reporting

no pandemic-related impacts in December 2021. Impacts related to

facility access restrictions eased by early Fall 2020, and by Summer

2021 less than one-fifth of employers reported restrictions. Termination

or amendment of revenue generating contracts persisted as an issue

through most of 2020 for over 40% of employers but declined through

2021. Supply chain disruptions, which were reported by nearly half of

employers during Summer 2020, have persisted for at least 30% of

employers through most of 2021.

DB_2022-002 chart 05: COVID-19 impacts to business operations (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2022-002 chart 06: COVID-19 impacts to business operations (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

The percentage of employers reporting supply shortages declined from 69%

in 2020 to 54% by the end of 2021. In 2020, personal protective

equipment was the most commonly reported supply shortage (62% of

employers), and in 2021, IT supplies were the most commonly reported

supply shortage (31% of employers). The percentage of employers

reporting supply shortages edged up between mid and late-2021 for field

supplies, lab supplies, IT supplies, office supplies, and other supply

shortages.

DB_2022-002 chart 07: Supply shortages needed for work or research (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

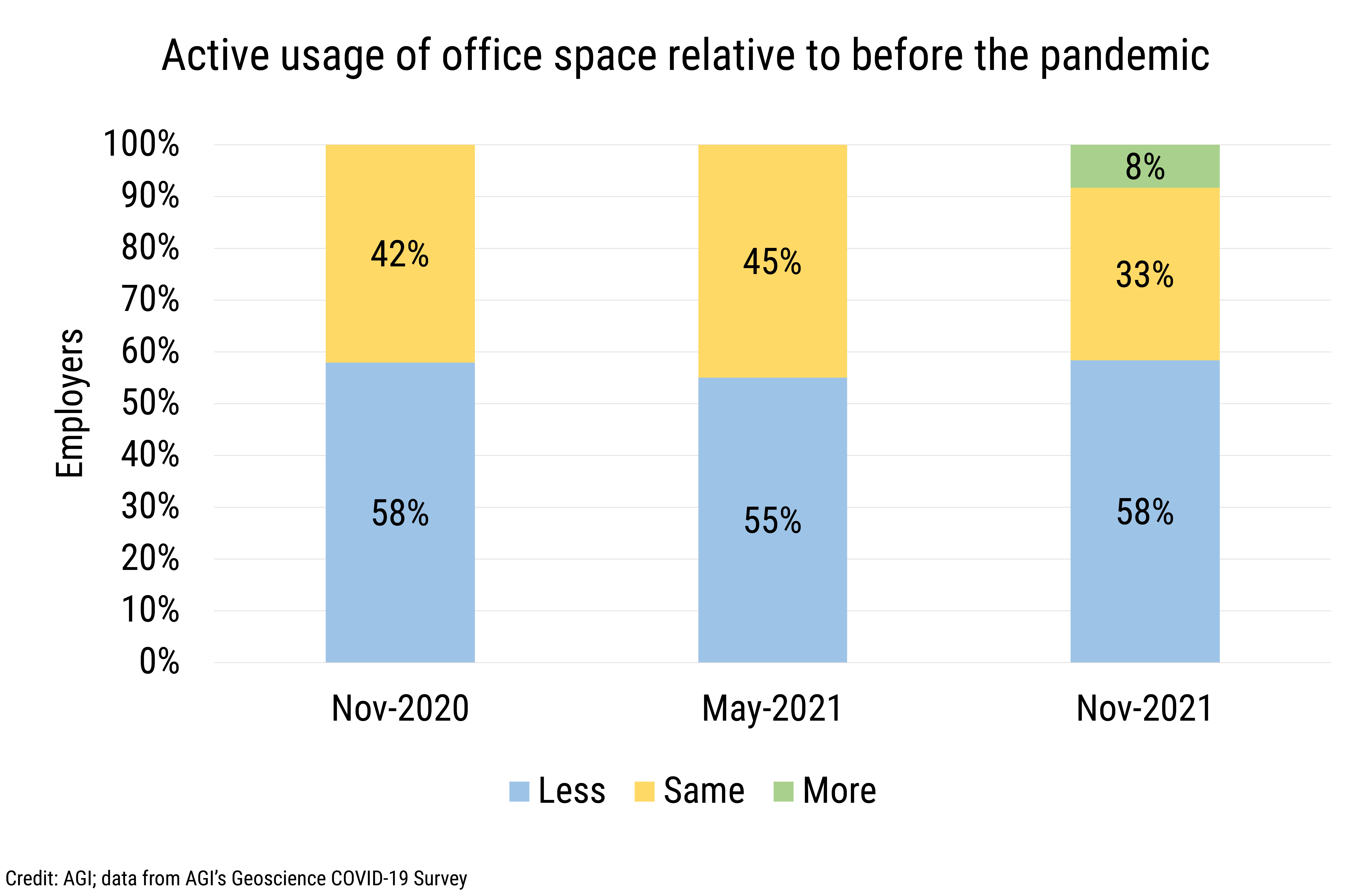

Changes to Work Environments

With the shift to remote work environments, over half of employers

reported reduced use of their office space. Three quarters of employers

reported using multiple technology platforms for conducting work, with

Zoom and Microsoft Teams being the most commonly reported platforms in

use (81% and 65% of employers respectively).

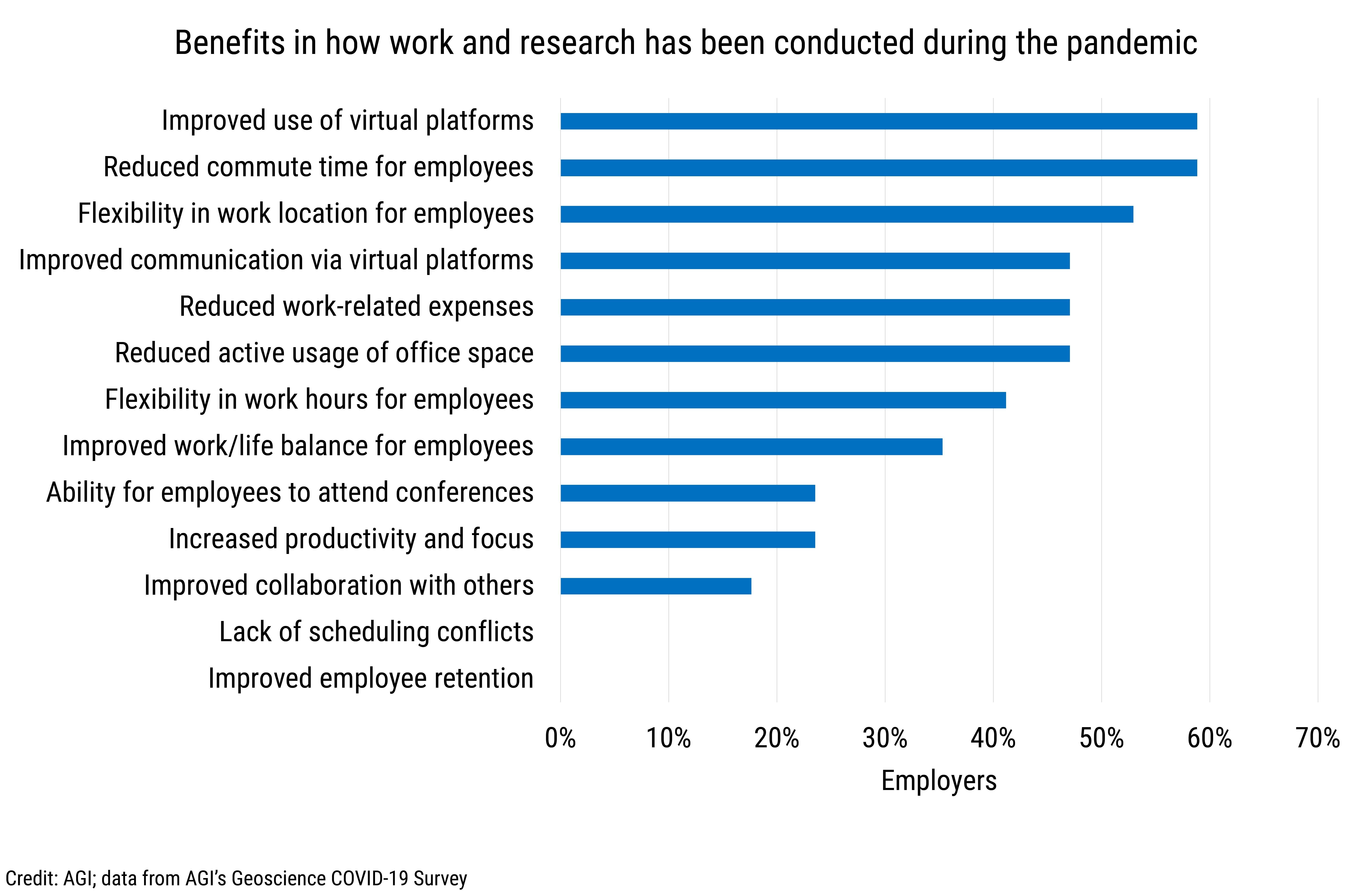

When asked about benefits to work and research during the pandemic, over

half of employers noted improved use of virtual platforms as well as

benefits to employees such as reduction in work commutes and flexibility

in work locations. In addition, over 40% of employers noted reduced

work-related expenses, reduced active usage of office spaces, and

flexibility in work hours for employees as benefits. It is interesting

to note that despite the improved use of virtual platforms and

flexibility in work location and hours noted by employers, lack of

scheduling conflicts and improved employee retention was not noted by

employers as benefits related to current work and research formats.

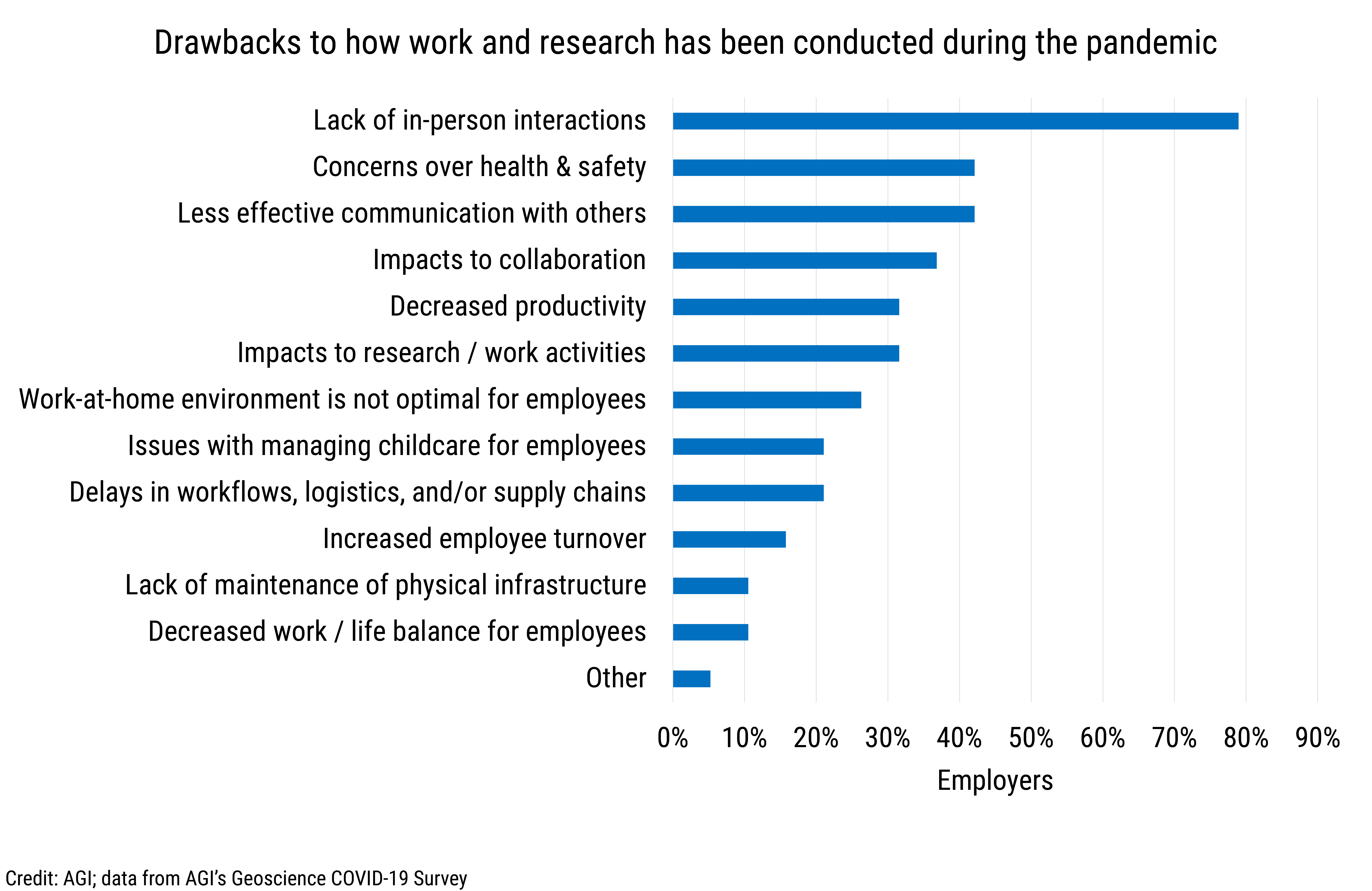

Despite the benefits from the way work and research has been conducted

during the pandemic, lack of in-person interactions has been the most

frequently reported challenge, with 79% of employers noting this issue.

In addition, over one-third of employers reported challenges related to

collaboration, less effective communication, and concerns related to

health and safety.

DB_2022-002 chart 08: Active usage of office space relative to before the pandemic (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2022-002 chart 09: Benefits in how work and research has been conducted during the pandemic (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2022-002 chart 10: Drawbacks to how work and research has been conducted during the pandemic (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

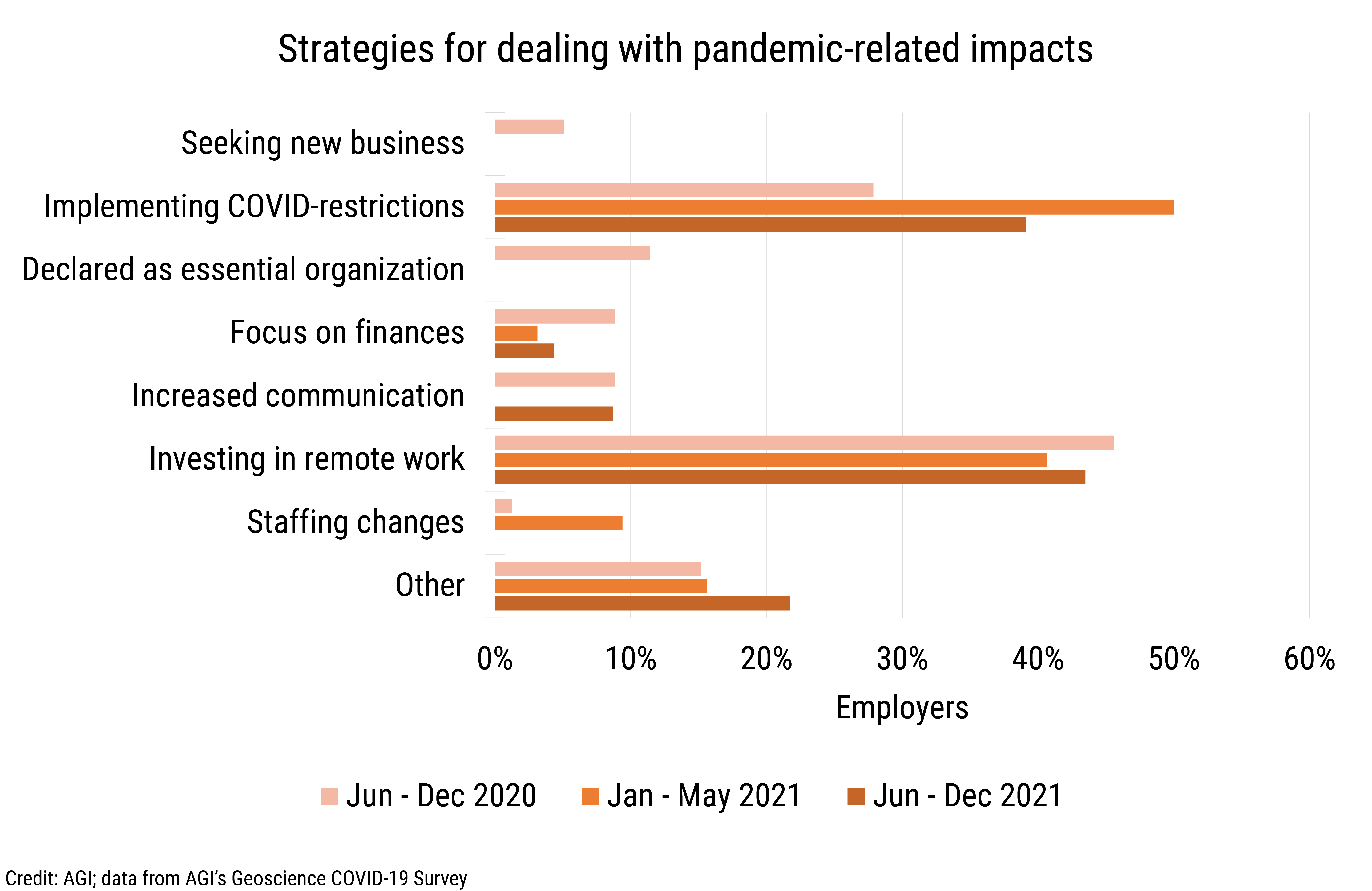

Strategies and Concerns

Strategies for dealing with pandemic-related impacts have primarily been

focused on investments in remote work resources and implementation of

health and safety protocols for those working in facilities, offices,

and at field sites. Other strategies noted by employers included more

flexibility in working environments, increased automation in business

operations, and prioritizing work to maintain operations and production.

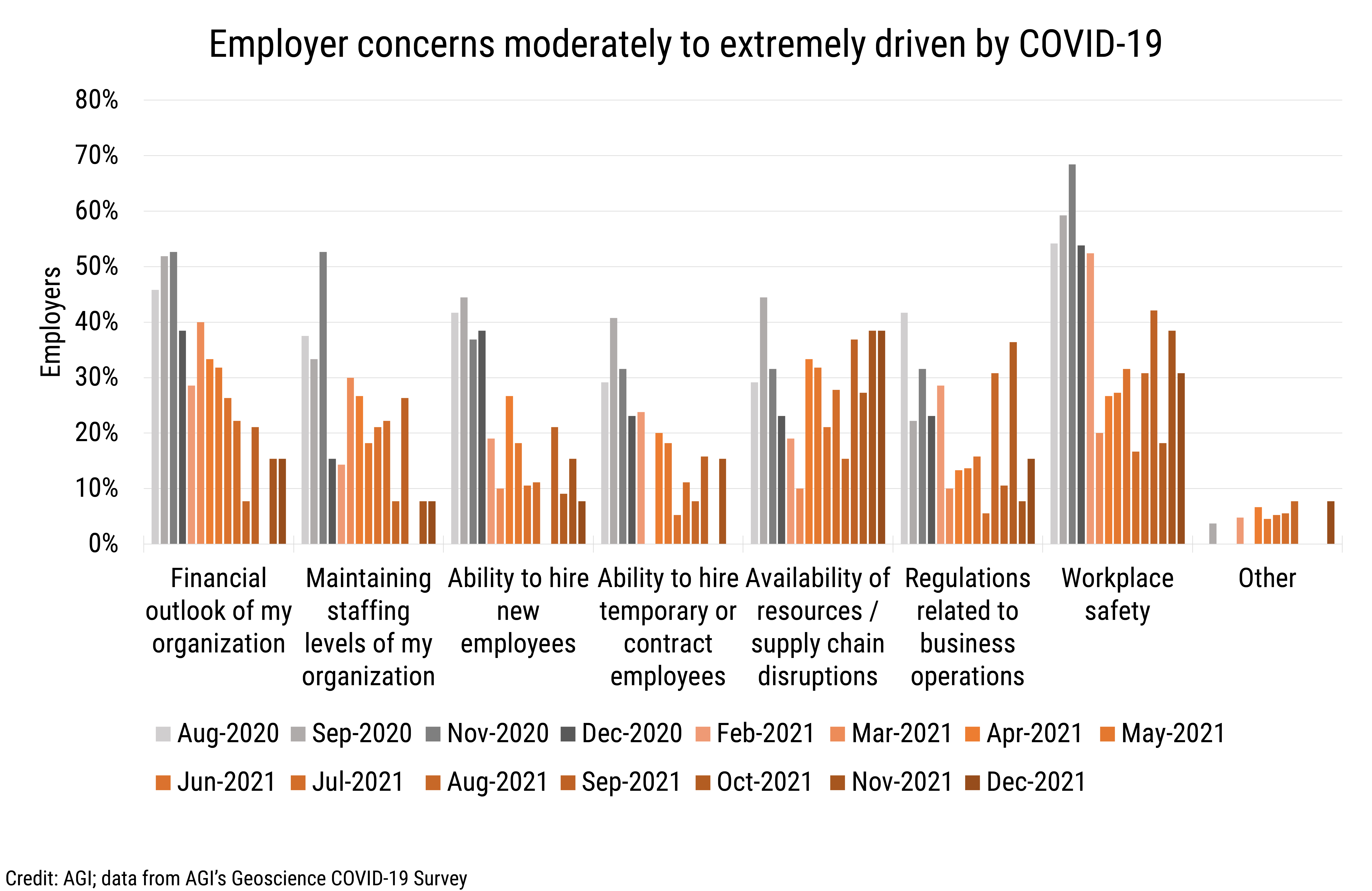

Since 2020, pandemic-driven concerns of employers have decreased across

all categories except those related to supply chain disruptions. In

December 2021, 38% of employers noted supply chain concerns driven by

the pandemic. Meanwhile, the percentage of employers noting concerns

related to workplace safety, which has been a major concern for most of

the pandemic, declined from 52% in February 2021 to 31% in December

2021.

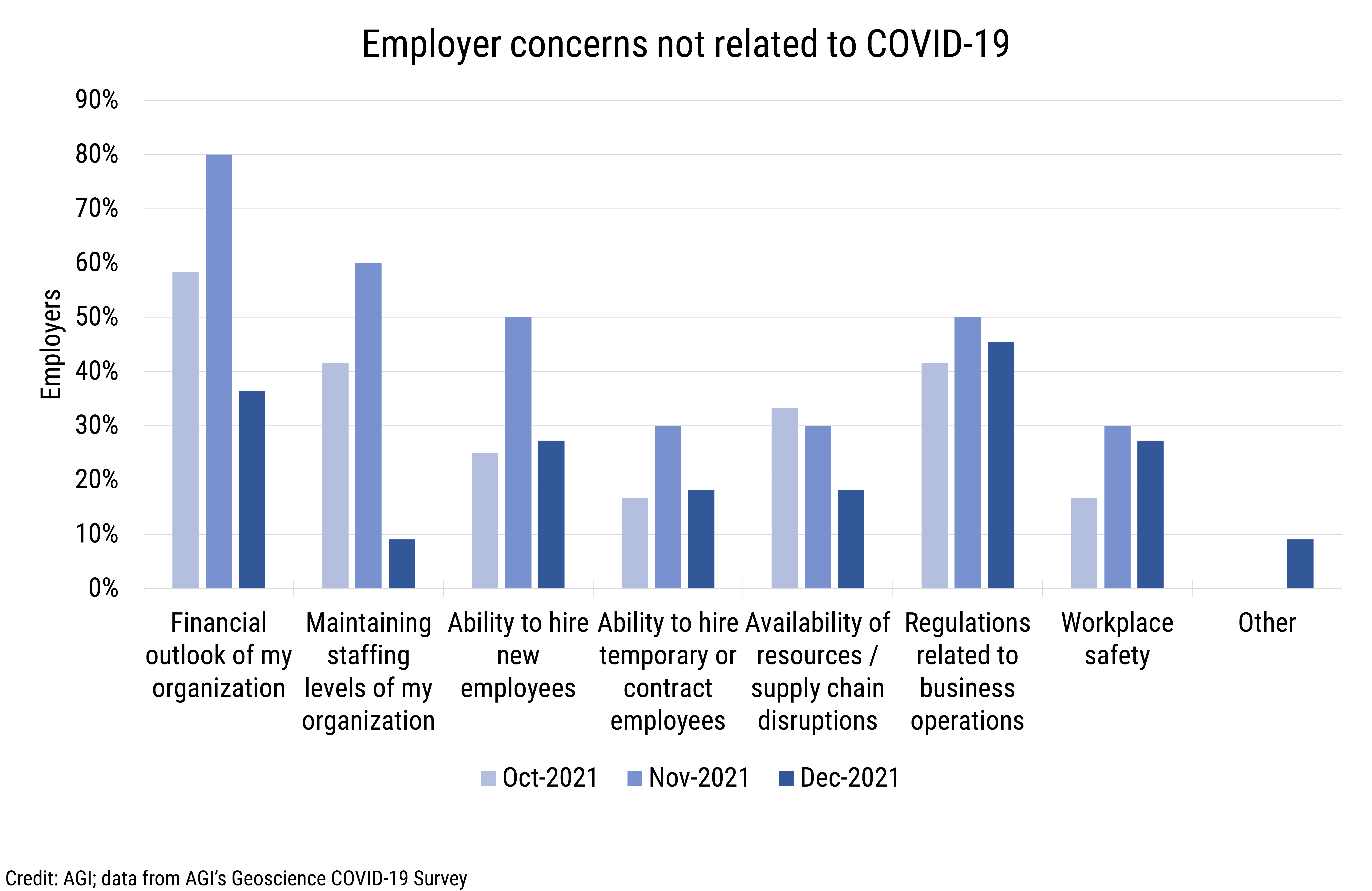

In October 2021, we began asking about non-pandemic concerns to

ascertain other issues that have begun to arise as the pandemic

continues. While the percentage of employers reporting non-pandemic

related concerns peaked in November 2021, there was a general decline

across most concerns since then, except for business operations

regulations and workplace safety. We will continue to monitor

non-pandemic related concerns in the coming months.

DB_2022-002 chart 11: Strategies for dealing with pandemic-related impacts (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2022-002 chart 12: Employer concerns moderately to extremely driven by COVID-19 (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2022-002 chart 13: Employer concerns not related to COVID-19 (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

We will continue to provide current snapshots on the impacts of COVID-19

on the geoscience enterprise throughout the year. For more information

about the study, please visit:

www.americangeosciences.org/workforce/covid19

Funding for this project is provided by the National Science Foundation

(Award #2029570). The results and interpretation of the survey are the

views of the American Geosciences Institute and not those of the

National Science Foundation.