Data Brief 2021-029 | October 18, 2021 | Written and compiled by Leila Gonzales and Christopher Keane, AGI

Download Data Brief

COVID-19 Impacts on Geoscience Business Operations, January – August 2021

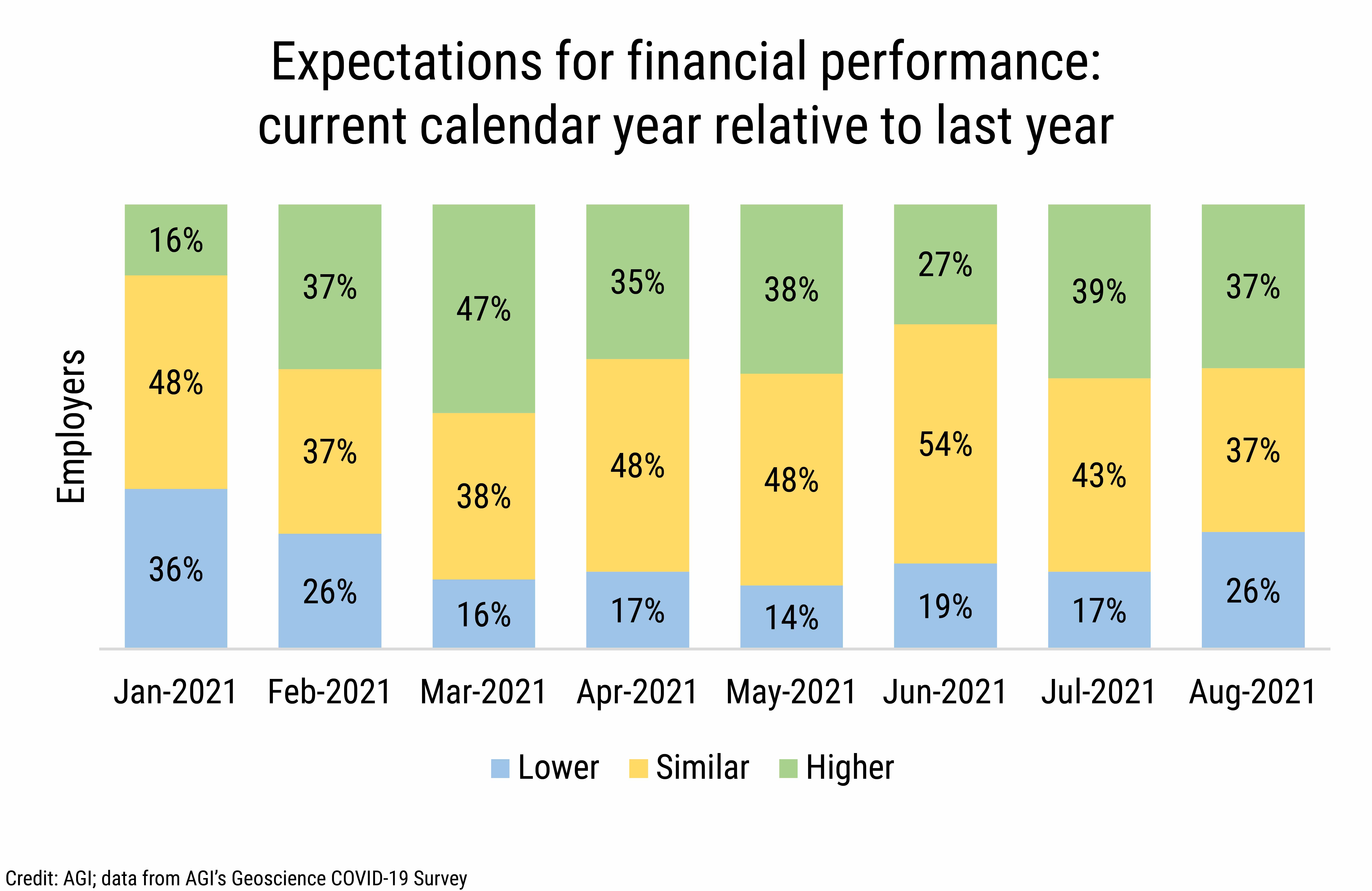

Between January and August 2021, over one-third of employers reported

expectations of better financial performance relative to 2020, and

between 37% and 54% of employers reported similar expectations of

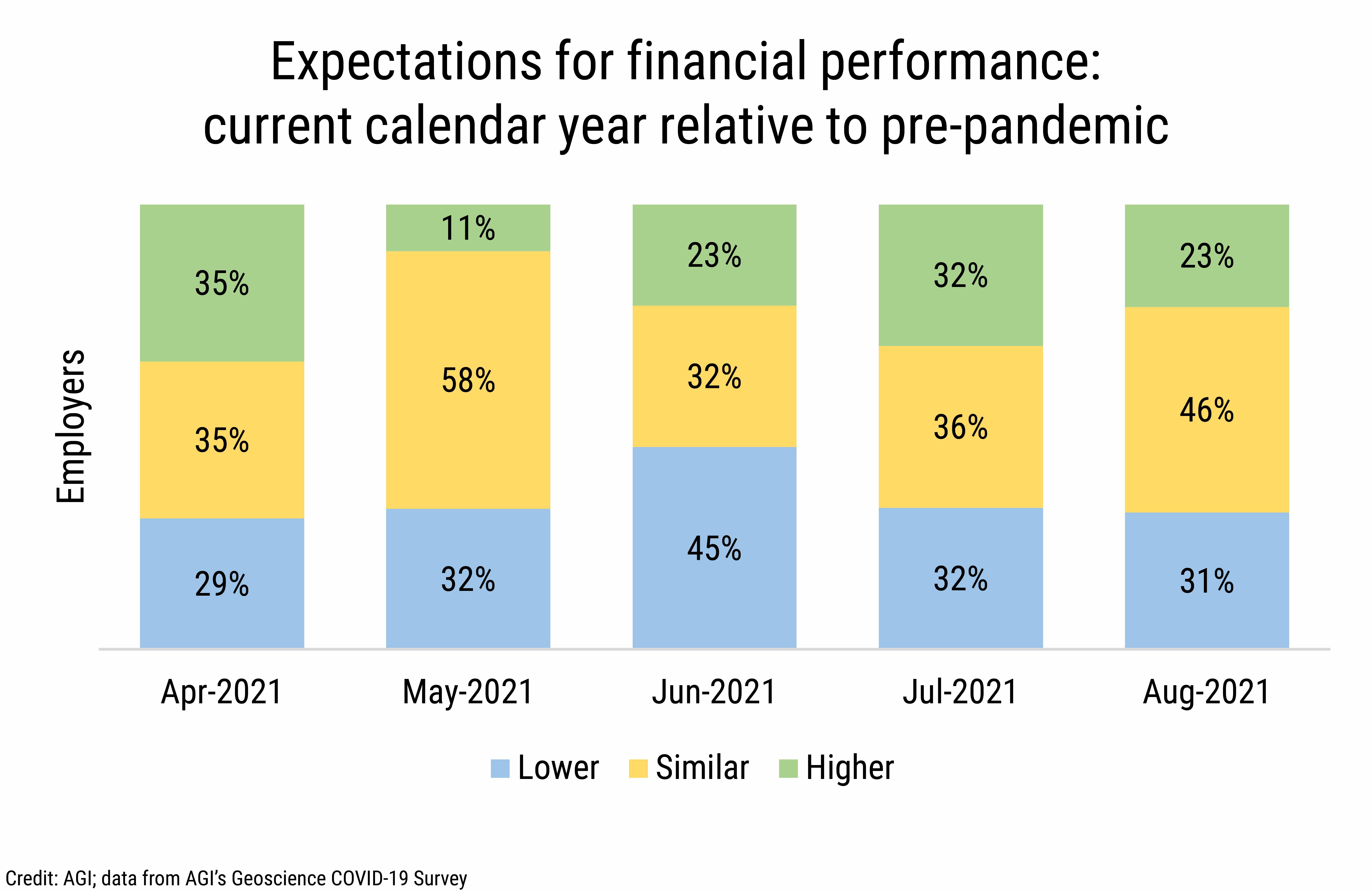

financial performance to 2020. By August 2021, nearly one-quarter of

employers reported expectations of better financial performance relative

to pre-pandemic times, and nearly one-third reported lower expectations

of performance.

DB_2021-029 chart 01: Expectations for financial performance: current calendar year relative to last year (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2021-029 chart 02: Expectations for financial performance: current calendar year relative to pre-pandemic (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

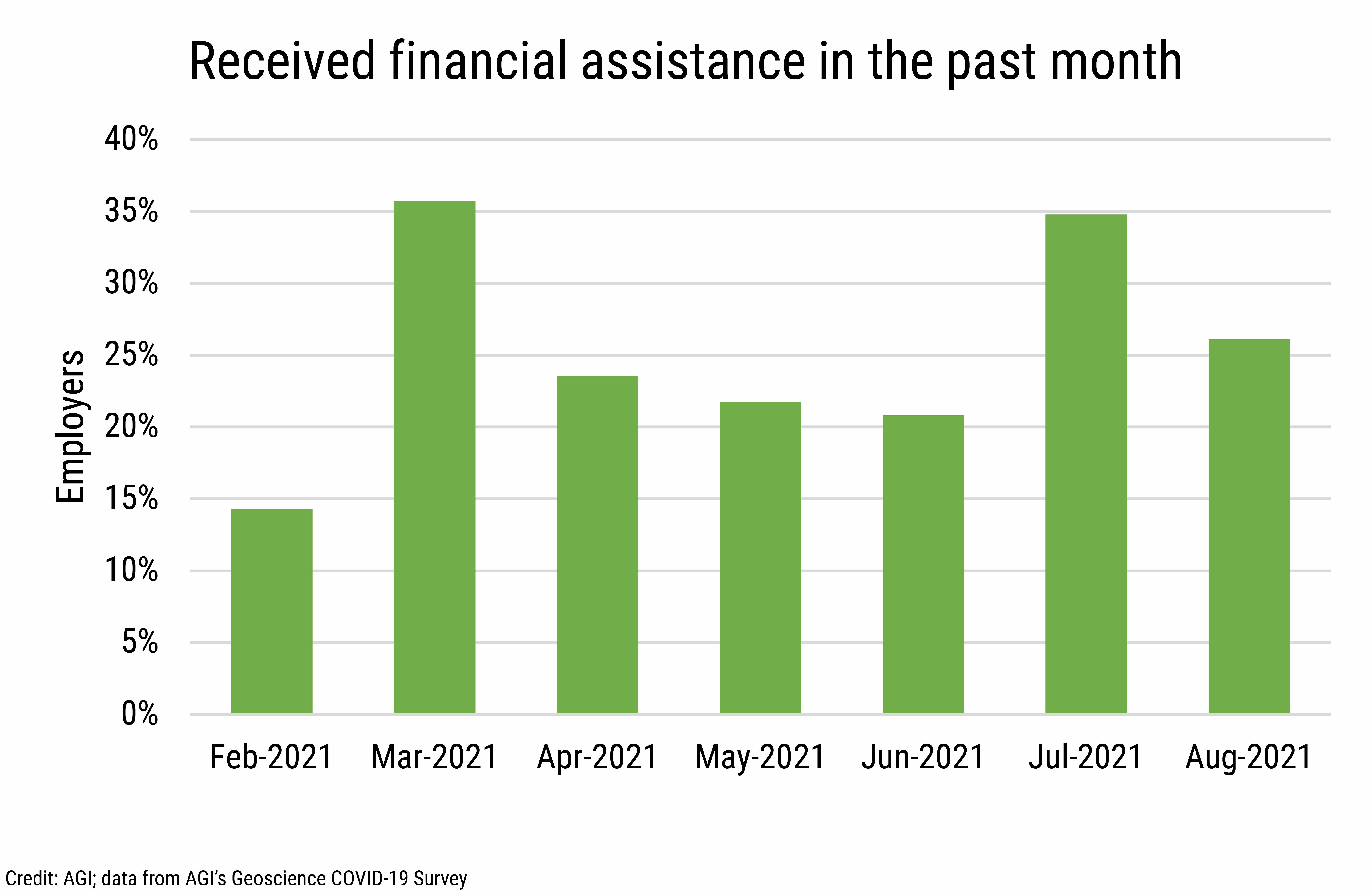

With the exception of March, July, and August 2021, less than

one-quarter of employers reported receiving financial assistance in

2021. Federal assistance comprised the majority of aid received,

followed by state and local aid, and then investment by business owners

into their companies.

DB_2021-029 chart 03: Received financial assistance in the past month (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

Productivity

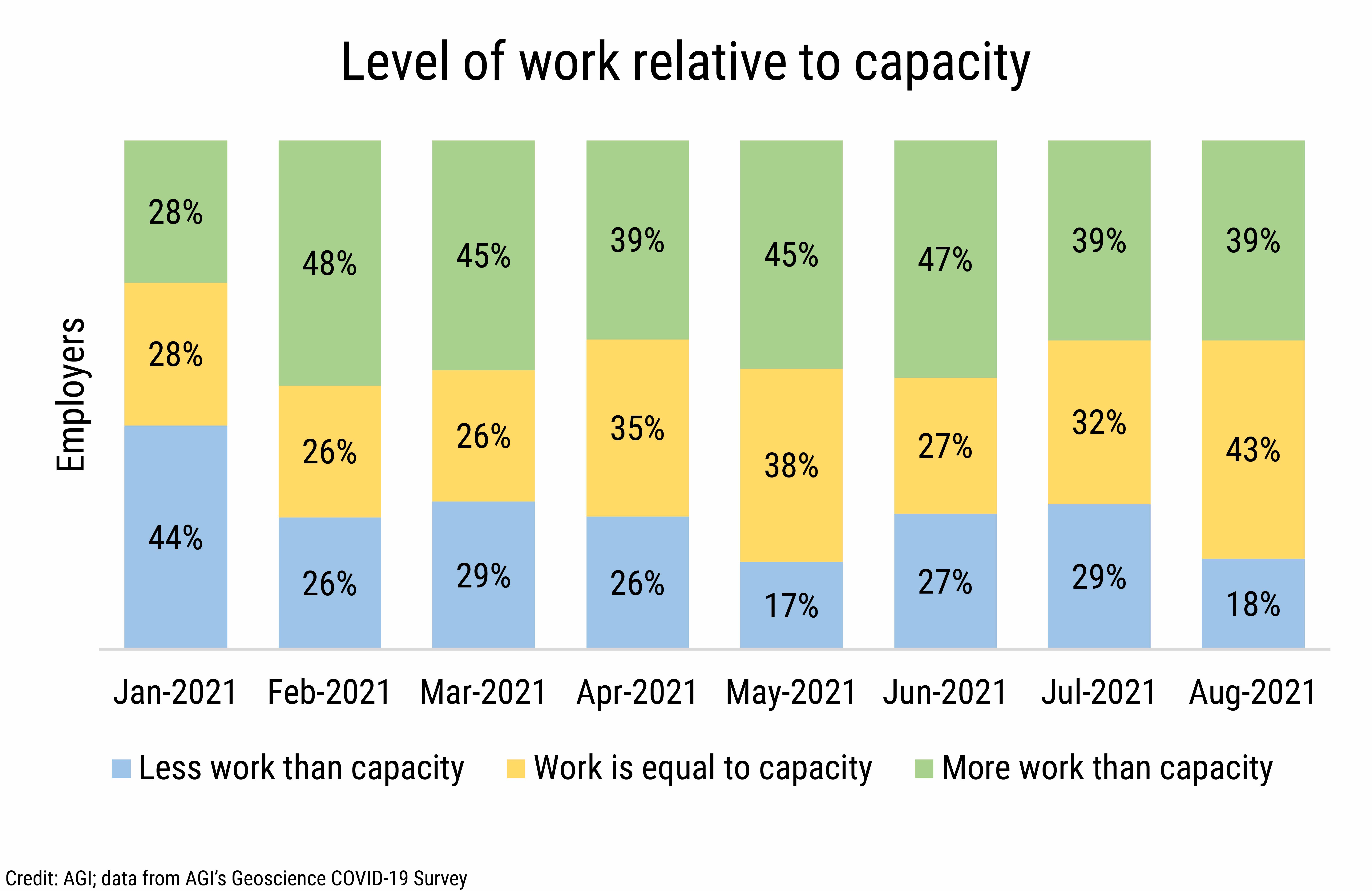

Since February 2021, just less than half of employers reported increased

workloads relative to staffing, which is an increase over 2020

productivity reporting. In May and August 2021, about 18% of employers

reported excess staffing capacity relative to workload, which was the

lowest since June 2020.

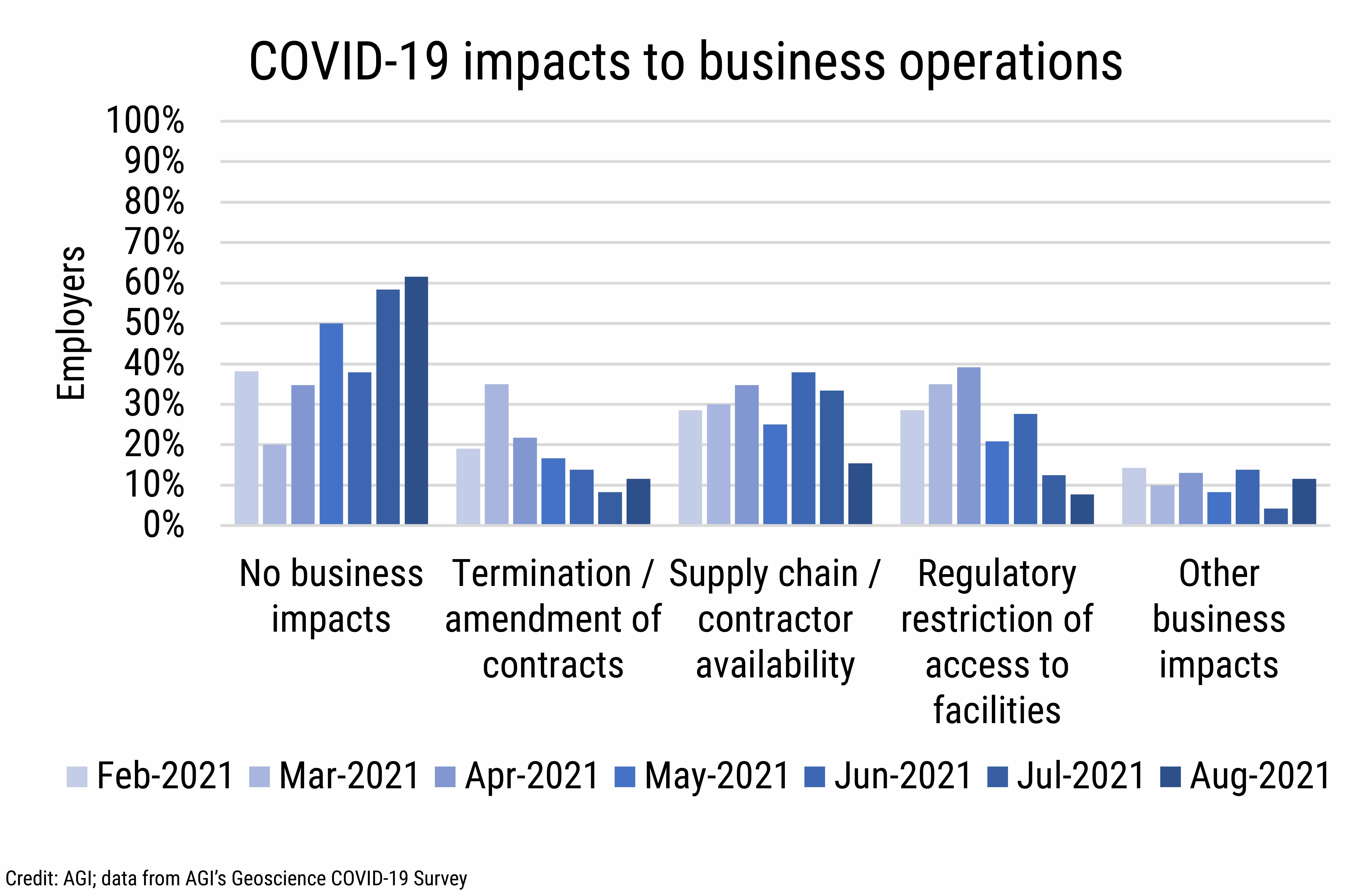

Through 2021, employers have increasingly reported no impacts on

business operations. The number of employers reporting termination or

amendment to revenue-generating contracts has declined, as has

regulatory restriction of access to facilities over the course of 2021.

Supply chain disruptions continued to impact over one-quarter to

one-third of employers through July 2021, but in August, this percentage

had declined to 15%.

DB_2021-029 chart 04: Level of work relative to capacity (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

DB_2021-029 chart 05: COVID-19 impacts to business operations (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

Strategies, Concerns, and Opportunities

Geoscience employers continued to deal with COVID-19 impacts in 2021

predominantly by investing in remote work resources followed by

implementation of health and safety protocols for those working in

facilities, offices, and at field sites. COVID vaccines, which were not

required by all employers responding to the survey, were listed as a

strategy by 18% of employers. Other strategies used by employers

included increased automation of operations to improve business

operation efficiencies, plans for permanent telework policies to reduce

operational costs and increase employee retention, re-prioritizing

workloads to maintain operations and production capacity, and reducing

overhead expenses where possible.

Employers commented on the benefits of virtual technology platforms in

reducing travel costs, increasing communication with clients both

domestic and international, and the efficiency platforms provide for

meetings and continuing education. Employers also mentioned issues

related to increased workloads to ensure efficient communication when

using virtual technologies. They also mentioned that there has been a

break-down in synergy from the lack of in-person communication, which

has been a common challenge among employers, academic departments, and

individuals throughout the pandemic. Some employers commented on the

impact to infrastructure which is not getting regular maintenance since

staff have not been regularly in the office.

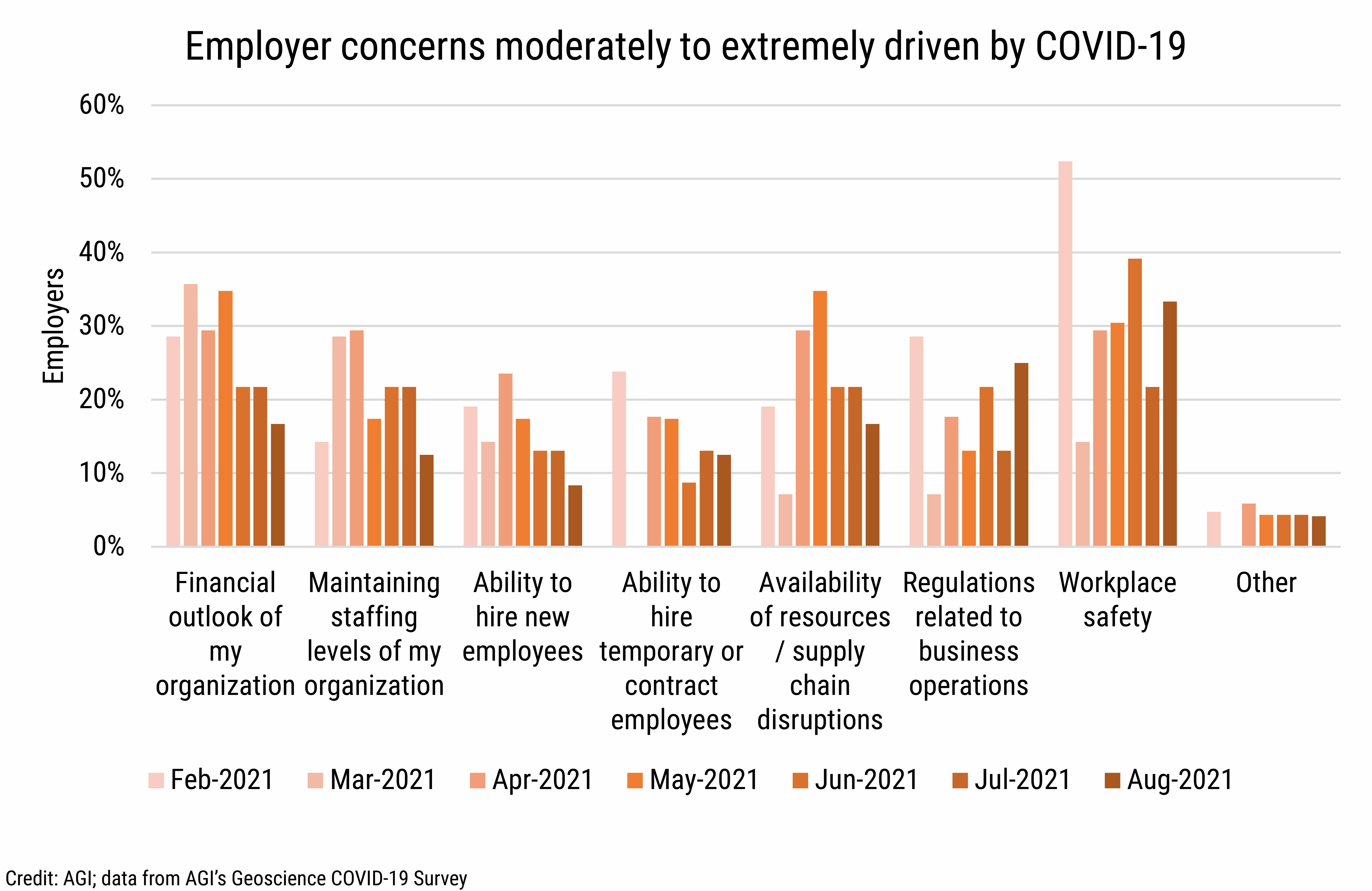

The most reported pandemic-related employer concern continues to be

workplace safety, with one-third of employers reporting this as a major

concern in August 2021. The percentage of employers reporting other

concerns driven moderately to extremely by the pandemic has declined

since January 2021, except regulations related to business operations,

which has increased. In addition, concerns over supply chain disruptions

peaked in May 2021, with just over one-third of employers reporting this

concern. All categories of concerns are down relative to December 2020

except for regulations related to business operations.

DB_2021-029 chart 06: Employer concerns moderately to extremely driven by COVID-19 (Credit: AGI; data from AGI's Geoscience COVID-19 Survey)

AGI

We will continue to provide current snapshots on the impacts of COVID-19

on the geoscience enterprise throughout the year. For more information,

and to participate in the study, please visit:

www.americangeosciences.org/workforce/covid19

Funding for this project is provided by the National Science Foundation

(Award #2029570). The results and interpretation of the survey are the

views of the American Geosciences Institute and not those of the

National Science Foundation.